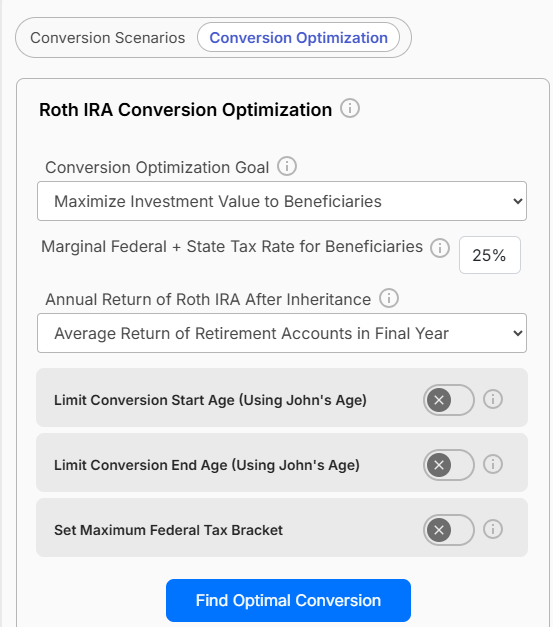

Roth Conversion Optimization for Beneficiaries

I want to optimize Roth conversions for my children to give them the most after-tax money possible.

How “Maximize the Investment Value for Beneficiaries” works

When you pick Maximize the Investment Value for Beneficiaries, the optimizer stops focusing primarily on your lifetime outcomes and instead prioritizes how much after-tax value your beneficiaries are expected to receive from what you leave behind.

That changes the math in two big ways:

- It evaluates outcomes from the beneficiary’s perspective (after their taxes).

- It converts future beneficiary dollars into present value, so it can fairly compare “value delivered” at different times.

1) It measures what heirs keep after their taxes

Traditional (pre-tax) retirement accounts usually create taxable income when withdrawn. Roth accounts generally create tax-free withdrawals (assuming qualified rules are met). So from an heir’s perspective, $1 in a Roth is often worth more than $1 in a Traditional account—because less of it is lost to taxes.

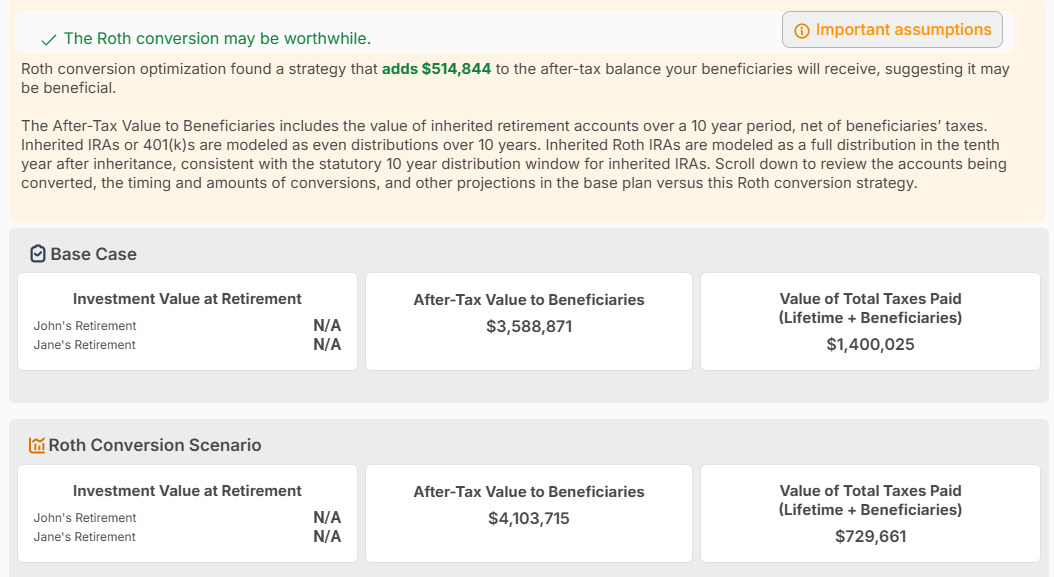

That’s why this goal can recommend more Roth conversion than a “minimize lifetime taxes” objective would: it may be worth paying some taxes during your lifetime if it increases the after-tax inheritance.

Entering the beneficiary tax rate

To model this, the tool lets you input an assumed beneficiary marginal tax rate (and sometimes state rate, depending on the setup). This is used as the estimated rate your beneficiary pays on taxable withdrawals they take from inherited pre-tax accounts.

- Higher beneficiary tax rate → Roth becomes more valuable → optimizer tends to favor more conversions

- Lower beneficiary tax rate → Traditional is less “penalized” → optimizer may recommend fewer conversions

Why marginal rate? Because inherited withdrawals generally “stack” on top of the beneficiary’s existing income. Using a marginal rate is a practical way to estimate the tax cost of each additional dollar they withdraw.

Tip: If you’re unsure, many people run it twice—once with a conservative (lower) rate and once with a higher rate—to see how sensitive the recommendation is.

How this works in practice

The Conversion Case (Roth): It assumes the heirs inherit a Roth account. They can let it grow tax-free for the full 10 years allowed by law and then withdraw the entire balance 100% tax-free. The tool calculates the value of that final, tax-free sum.

The Base Case (Traditional): It assumes heirs inherit a Traditional IRA. The tool models them taking distributions evenly over those 10 years and subtracts the income taxes the heirs would owe based on their projected tax brackets. The final number shown is the net after-tax value remaining for the heir.

2) Putting it together: how the optimizer scores each conversion path

For every potential conversion strategy, the optimizer roughly asks:

- What balances will be left to beneficiaries? (Traditional vs Roth)

- What is the expected tax cost to beneficiaries?

- Traditional withdrawals are reduced by the beneficiary tax rate you enter

- Roth withdrawals are generally not reduced (qualified assumptions)

- When do beneficiaries receive the money?

- What is the value of what they keep after taxes?

Then it picks the strategy with the highest investment value of after-tax beneficiary outcomes, subject to your constraints (conversion ages, bracket cap, IRMAA sensitivity, etc.).

Practical guidance for the beneficiary tax rate input

Here are common ways people choose a rate:

- Single beneficiary who’s a high earner: use a higher marginal rate assumption

- Multiple beneficiaries with mixed incomes: use a blended/average assumption

- Unknown future situation: run a low/mid/high scenario (e.g., 12%, 22%, 32%) and compare results

This goal is especially impactful when:

- You expect beneficiaries to be in higher brackets than you

- You want to reduce the chance they inherit a large pre-tax balance that creates big taxable withdrawals

- Legacy value matters more than minimizing taxes during your lifetime